Column

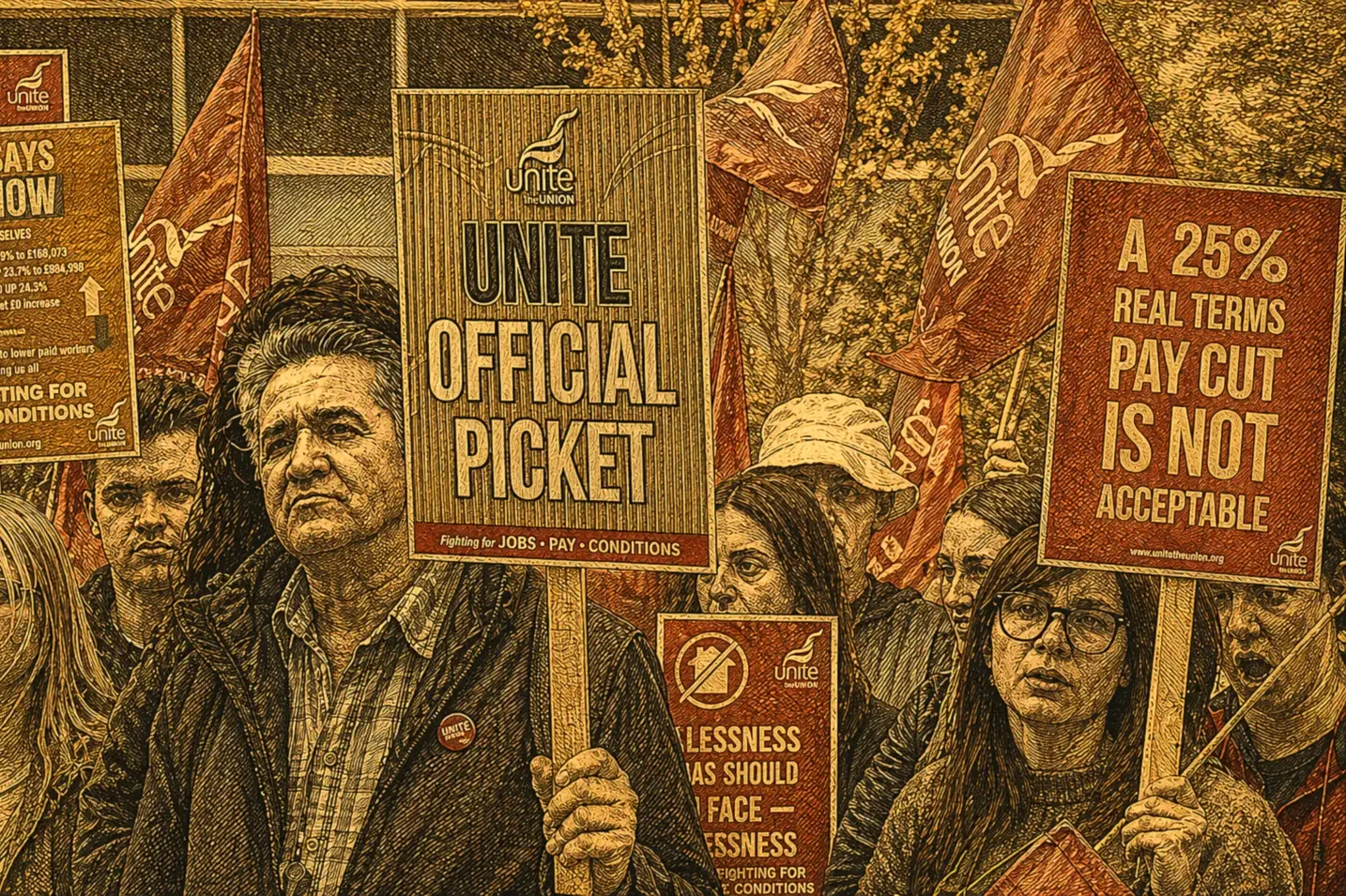

AI-Driven Power Dynamics: A New Era in the Long History of U.S. Labor Rights

The article argues that today’s difficult job search is not a temporary Gen Z shock but a structural shift in bargaining power toward employers as AI reduces labor demand. After the post-COVID tech hiring boom, overhiring unwound into layoffs and tighter openings. Long jobless spells and weak outside options make workers quieter at work. As automation substitutes for routine tasks, workers accept weaker pay and terms, cling to jobs out of fear and report burnout.

It situates this in a longer U.S. arc where labor protections expanded in the mid-20th century then eroded after the 1980s as unions weakened and capital gained leverage. AI is framed as an accelerant that can decouple growth and profits from job creation. The piece calls for policy responses including UBI, UBE and sovereign wealth dividends to restore baseline security and worker bargaining power.

The Limitations of Means Tested Programs: Unemployment Benefits Won’t Solve Job Seekers' AI-Driven Labor Market Struggle

The article argues that rising inequality and longer jobless spells are exposing the limits of means-tested support. Unemployment Insurance reduces poverty, but weekly benefits rarely match living costs and coverage often ends before many searches do. Programs like the EITC require recent earnings, so households can fall through gaps once UI expires, even with other safety-net programs.

It argues that baseline security should be a rule, not an exception tied to narrow eligibility windows. The alternative is a three-part architecture with a UBI that avoids cliffs and time limits, UBE that offers a standing public job option and sovereign wealth dividends that return part of AI-linked tax gains. Firms can train graduates and hire more deliberately, but the core claim is that durable protection in an AI labor market requires policy.

The Ghost of 1995: Why Powell's Bid for a "Soft Landing" Is Far Riskier Than Greenspan's

In our business, precision is power. We build predictive models for clients making some of their biggest fiscal decisions. A couple of months ago, one of our best performers, a model that had nailed inventory needs quarter after quarter, started to drift. Its forecasts weren’t wrong, exactly. Just… fuzzier. The prediction intervals widened. The signals got noisier.

When we investigated, the culprit wasn’t the math; it was the map. Our assumptions, built on decades of reliable data from America’s gold-standard statistical agencies, were suddenly out of sorts. Tariff tremors, policy-driven supply distortions, and even now a federal shutdown have all disrupted the data we depended on.

Embrace AI or Fall Behind? Actions for Companies, Recent Graduates, and Governments in an Age of Job Scarcity

As Kent and I highlighted two weeks ago, conventional recession indicators suggest a healthy economy, though recent trends in the labor market for college graduates paint a different picture. We pointed to some appalling anecdotes and statistics, including the case of the Computer Science major who submitted 5,762 job applications, only to hear back from none.

This reality begs the question of whether job creation in the age of AI will ever speed up as individuals, companies, governments, and educational institutions adapt. If so, when?

When the Degree Doesn’t Open Doors: The Employment Crisis Facing Young Graduates

In 2025, if you asked the average economist about the U.S. labor market, the answer might sound reassuring: the unemployment rate is holding steady around 4%, inflation is relatively under control, and job growth continues month after month. But ask a 23-year-old college graduate with a crisp new diploma and a browser full of unanswered job applications, and you’ll hear a different story.

The Mirage of the Market: Why Highs Don’t Mean Broad Prosperity

Earlier this year, John, a seasoned professional with a major firm, decided it was time for a leap. The stock market had been climbing steadily, financial headlines were full of optimism, and investor sentiment seemed to signal a revitalized economy. And John was getting increasingly tired of feeling left out. So, convinced that growth had returned, he left his stable job to join a consumer–facing start‑up.

Six weeks later, John was unemployed.

Why an Independent Fed Matters More Than Ever

Among colleagues who follow the U.S. economy closely, shifts in policy direction don’t usually come as a surprise. Yet, in recent weeks, a series of reports has indicated that the administration aims to select the next Federal Reserve Chair chiefly for ideological loyalty, favoring a candidate inclined to reduce interest rates regardless of macro dynamics; the prospect has given both these authors a pause.

As trained monetary and financial economists, we’ve spent years studying the delicate architecture that allows the Federal Reserve to function independently from political pressures. When that independence is threatened, so too is the foundation of macroeconomic stability.