Housing Affordability's Hidden Third Variable

by Mardoqueo Arteaga

AI;DR: Housing affordability has been analyzed, and experienced, as a two-variable problem: home prices and mortgage rates. Climate insurance is a third variable of similar magnitude that few housing models account for, that neither CPI nor PCE adequately captures, and that insurance markets are already pricing faster than home prices are adjusting. For buyers and renters making decisions today, that gap is no longer theoretical.

For the past three years, housing affordability has been understood primarily as a function of two forces. Home prices rose sharply during and after the pandemic. Mortgage rates then rose sharply to contain inflation. The interaction between these forces produced what researchers at the Federal Housing Finance Agency have called the lock-in effect: the freezing of housing turnover as millions of homeowners, sitting on sub-4 percent mortgages, declined to list their properties and reenter the market at rates more than double what they had locked in. FHFA research estimates that the lock-in effect was responsible for a 57 percent reduction in home sales at its peak. NBER research found that mobility among mortgaged households fell by 16 percent during 2022 and 2023.

Earlier this year, a structural shift had begun. The share of homeowners holding mortgages above 6 percent finally surpassed the share holding rates below 3 percent, which is a reset that signals the financial penalty for moving is gradually diminishing, even as the Iran conflict and elevated bond yields pushed rates back above 6.4 percent during the spring selling season.

What this two-variable frame misses is a third force that has been building throughout this period, largely outside the analytical models most economists and households use to evaluate housing decisions. Climate insurance in the form of its cost, its availability, and in a growing number of markets, its absence, is becoming a first-order input into housing affordability. It operates independently of Federal Reserve decisions and does not appear cleanly in the inflation measures used to track the cost of living.

The Scale of the Insurance Shock

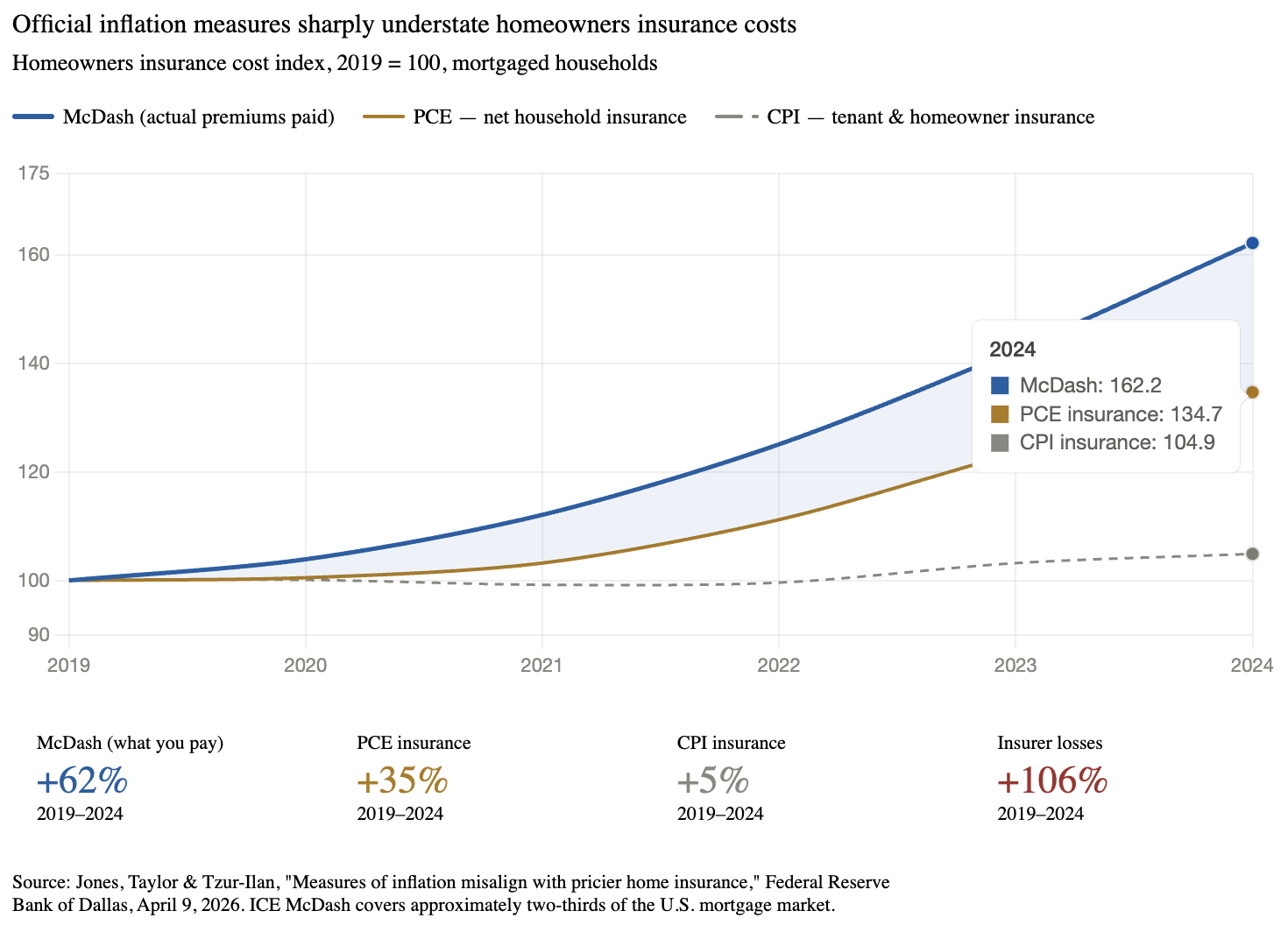

The numbers warrant attention on their own terms. According to ICE McDash data covering approximately two-thirds of the U.S. mortgage market, homeowners insurance premiums rose 62 percent between 2019 and 2024. The average mortgaged homeowner spent roughly $2,300 on homeowners insurance in 2024, or about 2.7 percent of median household income, up from approximately 2 percent before the pandemic. National averages, however, mask significant regional divergence. Premium growth reached 73 percent in Texas, 78 percent in Florida, 84 percent in Idaho, and 90 percent in Utah over the same period.

Several forces are driving these increases. During the pandemic, rebuilding costs surged as labor shortages and supply-chain disruptions pushed up construction prices. But the deeper driver is the rising frequency and severity of climate-related catastrophe losses. Between 2019 and 2024, insurer losses more than doubled, rising 106 percent over the period. Insurers increasingly rely on reinsurance to manage the correlated risk that large-scale disasters generate; reinsurance rates themselves increased 107 percent between 2019 and 2024, a cost that passes directly into the premiums homeowners pay.

Since mortgage lenders require homeowners' insurance as a precondition for financing, the insurance market is a direct participant in every home transaction. The consequences are measurable. In a 2026 survey of home buyers and sellers, nearly half reported encountering issues with homeowners' insurance, and 21 percent reported that a transaction fell through because of it. In Louisiana, estimates suggest that 30 to 40 percent of mortgage loans fail to close because insurance costs have made the transaction infeasible. California's FAIR Plan, which we can think of as the state's insurer of last resort, grew from approximately 200,000 residential policies in 2020 to around 450,000 by 2024 as private insurers exited the market. Nationally, the combined market share of FAIR plans and beach plans nearly doubled between 2019 and 2023.

The Measurement Gap

Despite a 62 percent increase in homeowners insurance premiums since 2019, neither CPI nor PCE fully reflects this growth. A working paper published by the Federal Reserve Bank of Dallas in April 2026 found that homeowners insurance is "becoming less affordable, yet this deterioration in affordability is not well captured by either of the most widely used inflation measures—CPI or PCE—both designed to track price levels rather than affordability or household financial strain."

I argue this divergence is methodological. The CPI's insurance component is constructed using renters insurance policy prices; coverage for personal belongings that costs a fraction of a typical homeowners policy and has trended very differently. The result is that the CPI tenant and homeowner insurance component rose only 5 percent between 2019 and 2024, against the 62 percent increase that mortgaged households actually experienced. PCE takes a different approach, measuring insurance as the net service it provides: premiums minus expected loss payouts. When insurer losses doubled between 2019 and 2024, as they did, the PCE net measure recorded only a 35 percent increase while actual premiums paid rose 62 percent. The gap between these figures from 5 percent to 35 percent to 62 percent is the distance between what inflation measurement is designed to capture and what households are experiencing.

The result is a structural gap between experienced housing costs and measured inflation. Households in high-risk markets are absorbing insurance cost increases on top of elevated mortgage rates, which our dear reader may think of as a compound affordability shock that does not register in the headline numbers that inform monetary policy, housing policy, or most financial planning models. Insurance costs may pass through to renters if landlords raise rents to cover higher premiums, but Federal Reserve Board researchers find this pass-through is very low, with a 75 percent increase in commercial property insurance corresponding to a modest less than 0.1 percent of total PCE inflation over the 2019–2024 period.

The Mispricing Problem

The third dimension of this issue is perhaps the most consequential for long-run asset values. Research by Wharton economists Parinitha Sastry, Ishita Sen, and Ana-Maria Tenekedjieva (which, by the way, were awarded the 2025 Marshall Blume Prize in Financial Research) finds that climate risk is being mispriced in both property insurance and mortgages. Insurance markets, drawing on increasingly granular climate and catastrophe risk data, are repricing faster than the transactions they facilitate. In their framing, "the signal gets jammed", or households and lenders become more exposed to climate risk than the price signals they receive would suggest.

Home prices have not yet adjusted to reflect the underlying risk that insurance premiums are already pricing in. J.P. Morgan's analysis of this divergence concluded that home prices "do not yet fully reflect the risks, but they may begin to soon." If we look to the Sunshine state, Florida’s condominium markets offer early evidence of what that adjustment may look like: by mid-2026, prices had declined in 92 percent of these markets, in part because insurance costs had made carrying costs prohibitive for both existing owners and prospective buyers. The Senate Budget Committee has estimated that climate-related disasters could eliminate roughly 9 percent of the world's total housing stock value by 2050, or approximately $25 trillion.

What the Two-Variable Model Misses

The traditional framework for evaluating a home purchase compares total monthly ownership cost against equivalent rent, accounting for tax benefits, equity accumulation, and expected price appreciation. That framework has two primary inputs: home price and mortgage rate. Climate insurance introduces a third input of comparable order of magnitude that is volatile, geography-specific, and not reflected in the historical data on which most financial models are calibrated.

For buyers in markets where insurance costs are already high and rising (e.g., coastal areas, wildfire-prone regions, and a growing number of interior markets now exposed to flood, hail, and tornado risk), the two-variable model may significantly understate the true cost of ownership. The relevant calculation is additive: can a buyer afford the mortgage, plus an insurance premium that has risen 62 percent in five years, in a market where the official inflation measures tracking that cost show it rising by 5 percent.

Insurance markets now carry information about climate risk that home prices, in most markets, have not yet reflected. When that gap closes, as it is closing in Florida, the adjustment will not arrive nor appear slowly. It will arrive as a belief revision: concentrated, fast, and larger than the sequential repricing that had been expected.

Sources:

Jones, Rachel A., Reid Taylor, and Nitzan Tzur-Ilan. "Measures of Inflation Misalign with Pricier Home Insurance." Federal Reserve Bank of Dallas, April 9, 2026. [Primary source for all insurance index data.]

Sastry, Parinitha, Ishita Sen, and Ana-Maria Tenekedjieva. "When Insurers Exit: Climate Losses, Fragile Insurers, and Mortgage Markets." 2025 Marshall Blume Prize in Financial Research.

J.P. Morgan Private Bank. "How Climate Risk—and Losses—Are Creating High Prices for Home Insurance." May 2025.

Levy Economics Institute of Bard College. "A Premium Crisis: Climate Change Threatens Homeowner's Insurance, Housing, and Financial Stability." Policy Note 2026/2, April 2026.

U.S. Government Accountability Office. Federal Analysis of Homeowners Insurance Markets. February 2026.

Batzer, Ross M. and Jonah Coste. "The Lock-In Effect of Rising Mortgage Rates." FHFA Staff Working Paper 24-03, 2024.