Why 50 Million Homeowners Aren’t Moving

by Mardoqueo Arteaga

AI;DR: Most U.S. homeowners aren’t choosing to stay put, but instead are financially locked in. A 3% mortgage in a 6.5% world turns moving into a six-figure decision, freezing mobility across tens of millions of households. So instead of a normal housing supply shortage, we have a market that can’t clear: supply is constrained by incentives, not just construction. Until rates fall meaningfully (or the system itself changes), housing will remain a story of paper wealth held by real constraints, and a growing divide between those who can move and those who cannot.

During COVID, interest rates dropped to basically nothing. If you bought a house in 2020 or 2021, or if you refinanced during that window, you probably locked in a mortgage rate around 3%. Maybe lower. That was a once-in-a-generation deal. Your parents didn't get that rate. Your kids won't get that rate, probably.

Put some math behind it. At 3%, a $400,000 loan carries a monthly payment of about $1,686. At today’s rates, around 6.46%, that same loan costs roughly $2,530 per month. That is an $844 difference. Same house, same neighborhood, same commute.

Over a year, that gap is $10,128. Over ten years, $101,280. Over the life of the loan, it exceeds $300,000.

So what do you do? You stay. Even if the house doesn't fit your life anymore. Even if your family has grown. Even if you got a job offer somewhere else. Even if your parents need you closer. You stay, because leaving costs you a quarter million dollars over the life of the loan.

And here's the thing: fifty million households are making this exact same decision right now.

Locking In (Constraint)

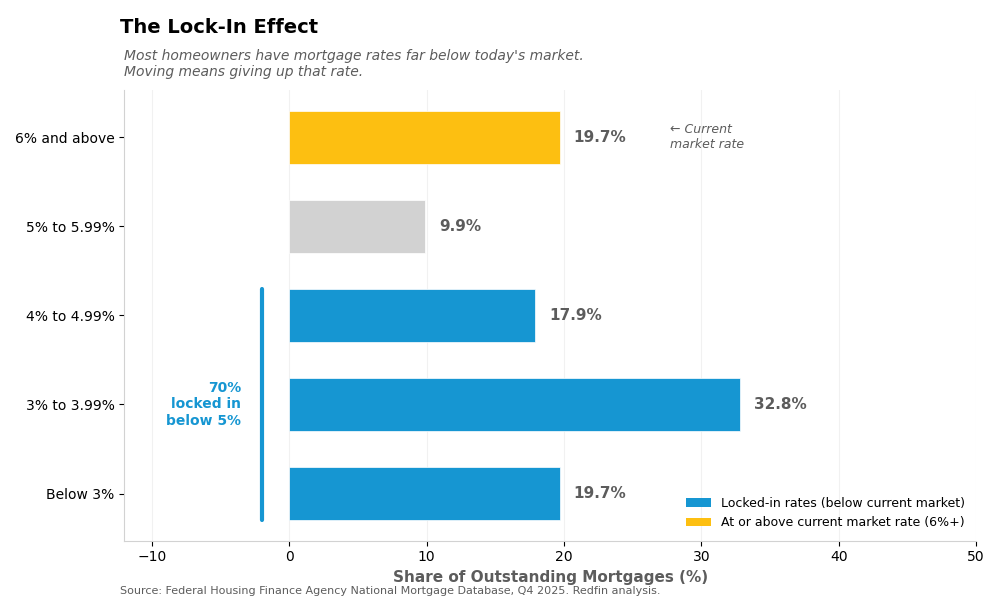

The Federal Housing Finance Agency (FHFA) tracks the distribution of mortgage rates across all outstanding loans. As of late 2025, over half of American mortgages carry rates below 4%. Nearly 20% are below 3%.

On the other side of the ledger, the share of mortgages above 6% has climbed to its highest level since 2015. The market is therefore bifurcated into two populations: those who locked in during the pandemic and the others.

For the locked-in majority, the behavioral effect is measurable. FHFA finds that each one percentage point increase in rate differential reduces the probability of selling by 18%. If you hold a 3% mortgage and face a 6% market, you are roughly 50% less likely to move.

Freddie Mac estimated that homeowners in their portfolio alone have locked in a collective $700 billion in savings relative to current market rates. That is $700 billion in value that evaporates the moment they sell.

Over half of mortgage holders have rates below 4%, while current market rates exceed 6%. The gap explains why so few are willing to sell.

A Market Without Sellers

The consequences of the lock-in effect show up everywhere else.

Existing home sales in 2025 fell to 4.06 million, the lowest annual total since 1995. March 2026 made it worse: sales dropped 3.6% month-over-month, now running at roughly 3.94 million annualized. That is below last year's already-weak pace. As NAR Chief Economist Lawrence Yun put it: "Lower consumer confidence and softer job growth continue to hold back buyers."

Yet prices keep rising. The median home price hit a new record for March. Yun noted that price growth has helped the typical homeowner accumulate $128,100 in housing wealth over the past six years. That is wealth they cannot unlock without surrendering their rate.

Inventory tells the same story. Earlier this year, there were 1.29 million homes for sale nationally, representing 3.8 months of supply. Before the pandemic, the typical level was closer to 2 million homes and five to six months of supply. The market remains structurally short.The National Association of Realtors notes the paradox: there are 6 million more jobs today than in 2019, yet home sales are down by 1 million per year.

If you're trying to buy your first home right now, you're facing the worst of all worlds. High prices, high rates, and almost nothing to choose from. You're competing with other buyers for a tiny pool of listings, and you're financing at rates your slightly-older coworker never had to deal with. It's not in your head. The market is genuinely stacked against you.

If you already own a home with a low rate, you're in a weird position. On paper, you're doing great. You've built equity. Your payment is locked. You're insulated from all the chaos. But you're also stuck. That equity is real, but it's illiquid. You can't access it without giving up the rate. You can't move without taking a massive hit. You're rich on paper and trapped in practice.

Even across segments, the effect is uneven. At the high end of the market, where buyers rely less on financing, activity has held up better. Luxury homes are less sensitive to mortgage rates, and in some cases, inventory has been more fluid. But for the broad middle of the market (where financing drives decisions), the lock-in effect dominates.

Life Happens Anyway

Over time, some movement returns. People still experience what real estate professionals call “trigger events”: marriages, divorces, job changes, children, retirements. These events force transactions even when rates are unfavorable. That is what we are mostly seeing now. Inventory has ticked up modestly, but this most likely reflects necessity, not choice.

At the same time, the locked-in cohort is not shrinking quickly. The share of mortgages below 4% declines by roughly one percentage point per year. At that pace, these households will shape the market for most of the decade.

Rates as the Transmission Mechanism

Mortgage rates had been drifting lower through late 2025. The average 30-year fixed rate fell from above 7% to around 6% by January 2026. Analysts were cautiously optimistic that mobility would improve as the gap between locked-in rates and market rates narrowed.

Then the Iran war began.

Geopolitical uncertainty sent bond markets into turmoil. The 10-year Treasury yield, which heavily influences mortgage rates, spiked. As of April 2, the average 30-year mortgage had climbed to 6.46%, marking the fifth consecutive weekly increase. Rates are now nearly half a percentage point higher than they were a month ago. The window of modest relief closed before most homeowners could act on it.

This is how geopolitics enters your budget: Narrative volatility feeds market volatility -> Market volatility feeds interest rate expectations -> And interest rate expectations feed directly into your mortgage rate. The chain from a news headline to your monthly payment is shorter than most people realize.

What Would Unlock the Market

The honest answer is that nothing will unlock the market quickly. Rates would need to fall below 5% to make moving rational for most locked-in homeowners. No major forecaster expects that in 2026 or 2027. The consensus range for year-end is 5.9% to 6.3%.

Even if rates reach 5.5%, the question is whether behavior actually changes. After years of elevated rates, expectations may have reset. Households may remain cautious, and mobility may recover more slowly than models predict. The response will likely vary by segment, with higher-end and cash-driven buyers moving first, and rate-sensitive households lagging.

Policy alternatives exist. Assumable mortgages and portable mortgages could reduce the penalty of moving by allowing borrowers to carry low rates with them. These structures exist in other markets, but are not standard in the U.S., in part because they complicate the securitization of mortgage debt.

In their absence, the adjustment will be gradual. New construction will add supply at the margin, as we have seen. Trigger events will continue to force transactions. But the core incentive remains intact.

The cost of moving is real. The cost of staying is tolerable. So they wait.

Sources:

Federal Housing Finance Agency. "National Mortgage Database: Mortgage Rate Distribution." FHFA, Q4 2025.

Coste, Jonah, William M. Doerner, and Michael Seiler. "The Lock-in Effect of Rising Mortgage Rates." FHFA Working Paper, 2024.

Freddie Mac. "Primary Mortgage Market Survey." Freddie Mac, April 2, 2026.

Freddie Mac. "Mortgage Rate Lock-In and the Housing Market." Freddie Mac Research, 2023.

National Association of Realtors. "Existing-Home Sales Report: March 2026." NAR, April 13, 2026.

Redfin. "Share of Mortgages with Rates Above 6% Climbs to 10-Year High." Redfin News, September 2025.

Wolf Street. "Update on the Lock-In Effect in the Housing Market." Wolf Street, March 2026.