A Growing Gender Divide in the AI Economy

by Kent O. Bhupathi

Last month, Melissa and I wrapped a white paper on a strange feature of the current economy. The usual recession script was not fully showing up where the NBER playbook would have led you to expect it. Instead, we were seeing pockets of counter-cyclicality and capital deepening that looked tied, at least in part, to the pressure wave from AI investment. Businesses were spending, reorganizing, and rethinking labor in ways that felt less like a normal cycle and more like an early structural shift.

What we did not have time to tackle in that paper was the gender question. And that omission started to bother me as one series after another crossed my desk.

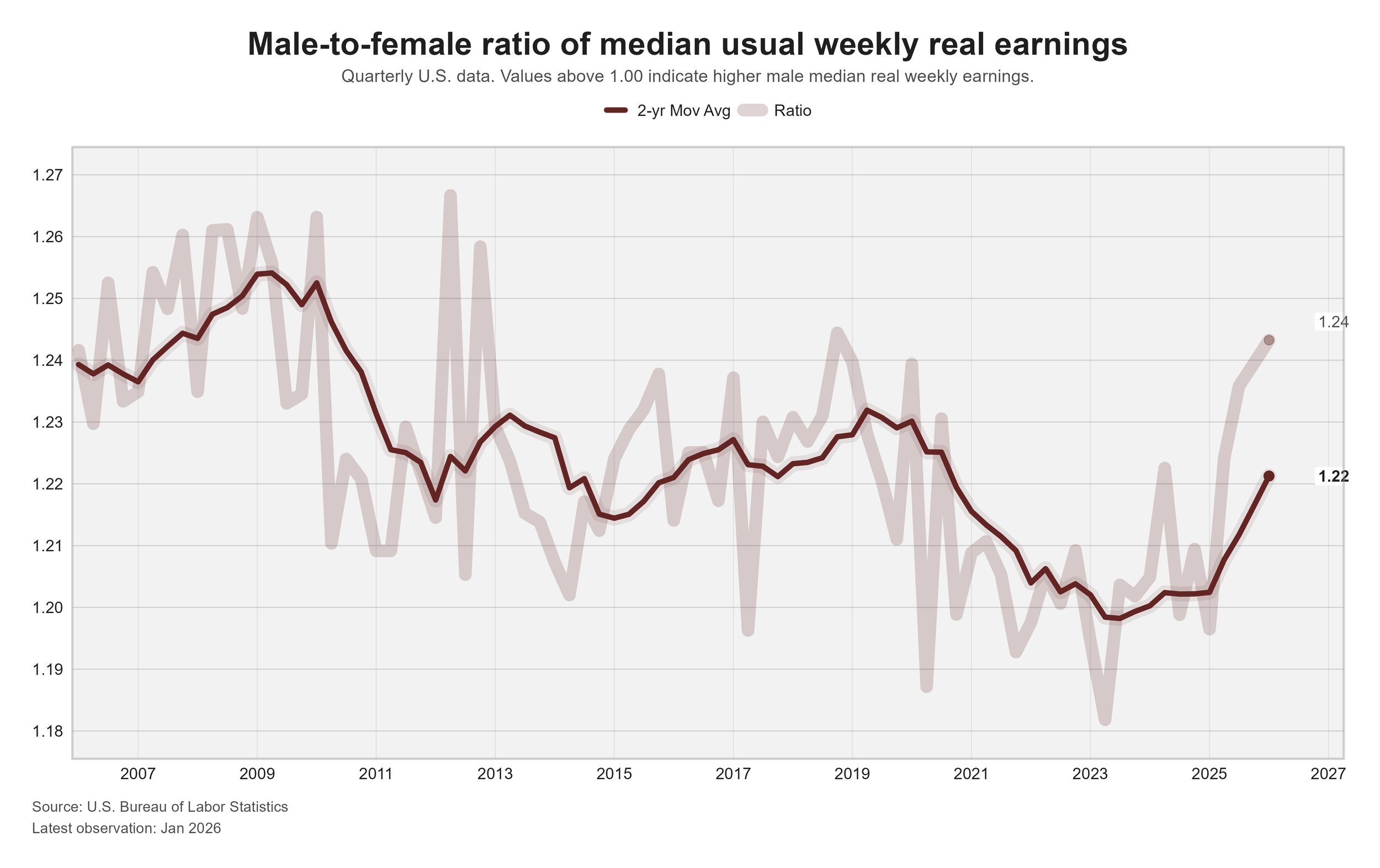

Male-female income inequality appeared to hit an inflection point in the second quarter of 2023. From there, the trend moved up, then jumped in 2025, reaching levels not seen since 2018 and not sustained since the Great Recession era.

We are still early in this story. And nobody serious should pretend the AI economy has already revealed its final social shape. But when a labor-market trend bends that sharply, it is worth asking whether the new investment regime is beginning to reshape who gets rewarded, who gets exposed, and who gets left standing in the wrong lane.

The current evidence does not support a neat, panic-friendly claim that AI has already blown open the overall U.S. gender pay gap. That would be too clean and, at this stage, too confident. What the evidence does show is more subtle and, frankly, more consequential. AI is already changing the architecture of inequality. Women are more likely than men to work in jobs exposed to AI. Men are more likely than women to use generative AI tools at work. Firms investing in AI are shifting toward more educated, more STEM-intensive, more IT-heavy workforces. So, while the wage data has not fully “broken” yet, the structure beneath it is definitely shifting.

And, to me, that distinction matters, since aggregate pay gaps are lagging indicators. By the time they flash red, the labor market has often been reorganized for a while.

The First Cracks Are Already Visible

Start with occupational exposure. On this point, the U.S. evidence is unusually consistent. Pew found that in 2022, 21% of women versus 17% of men were in the most AI-exposed jobs. Treasury’s 2024 analysis put the gap wider, with 29.2% of women in highly exposed occupations compared with 21.9% of men. And IMF research based on U.S. worker-level data reached the same broad conclusion, finding greater occupational exposure to AI among women and highly educated workers.

That exposure is not evenly spread across the economy. Brookings found that generative AI is especially consequential for clerical and administrative work, where women remain heavily overrepresented. Its estimates suggest 36% of female workers are in occupations where generative AI could save half of task time, compared with 25% of male workers. In another Brookings analysis drawing on work by Manning and Aguirre on adaptive capacity, 6.1 million highly exposed U.S. workers had low capacity to adapt if displaced, and 86% of them were women. This points to a much broader vulnerability across office work, especially in roles many companies still treat as routine support rather than as the foundation of a career.

Yet the story is not simply that women are exposed and men are safe. The exposure pattern splits in two. Treasury found that among college graduates, men are actually more likely than women to work in highly AI-exposed occupations, 38.9% versus 31.1%. But that gap has a straightforward explanation. Men remain more concentrated in AI-exposed majors and technical occupations such as engineering and computer science. So, ultimately, the jobs most likely to benefit from AI are not simply the ones that use it, but the ones that build it, customize it, supervise it, or sit close to the investment decisions around it.

This is where the labor-market logic gets uncomfortable. Women are more exposed in the aggregate because they are concentrated in clerical, administrative, and some professional office roles that AI companies are working to restructure. Men are more exposed at the technical end of the college-educated distribution because they are more concentrated in engineering, computing, and other AI-complementary fields. One side of the market faces automation pressure. The other stands closer to the complementarity premium.

More Exposed, Less Equipped

Then comes the most important asymmetry in the evidence. Even though women are more exposed overall, men are more likely to use generative AI at work.

Bick, Blandin, and Deming found that workplace generative-AI adoption in 2024 was 7.5 percentage points higher for men than for women. Their estimates imply usage rates of about 29.1% for men and 23.5% for women. A separate nationally representative survey analyzed by Bank for International Settlements researchers using the New York Fed’s Survey of Consumer Expectations found a larger gap, with 50% of men reporting generative AI use in the prior 12 months, compared with 37% of women. Demographics such as income, education, age, and race explained only a modest share of that difference. The biggest factor was self-assessed knowledge about generative AI, followed by privacy and trust concerns and differing views of its risks and benefits.

A broad synthesis by Otis, Delecourt, Cranney, and Koning, covering 18 studies and more than 140,000 individuals, found that gender gaps in generative-AI use are nearly universal. In U.S. samples, the gap often falls in the range of 10 to 20 percentage points.

Put that all together… and the risk becomes obvious. If AI mainly augments workers, women appear less likely to capture the early productivity gains. If AI mainly automates tasks, women are more concentrated in some of the roles most likely to be reorganized. That is just a terrible hand to be dealt…

And it gets worse if employers treat AI access as an informal perk for the already confident, already technical, already high-status worker. Markets can produce inequality without conspiracy… a pattern is enough.

What the Data Says So Far About Jobs and Pay

The good news, if we can call it that, is that the loudest public claims still outrun the strongest evidence on realized wage effects. The best U.S. studies do not show a large, clean, economy-wide AI shock to wages so far.

The clearest causal evidence on workplace deployment comes from Brynjolfsson, Li, and Raymond’s field experiment in a Fortune 500 customer-support setting. Workers given access to a generative AI assistant saw productivity rise by roughly 15%. Novice and less skilled workers benefited most, with novice workers improving by about 30%. The tool compressed the productivity distribution rather than simply showering gains on the stars. That result points to one channel through which AI could reduce inequality within occupations. But it does not show whether those gains reached wages or estimate gender-specific pay effects.

At the market level, Daron Acemoglu et al. tracked the near-universe of U.S. online vacancies from 2010 onward and found rapid growth in AI-related vacancies, lower hiring in non-AI positions at more exposed establishments, and changes in skill requirements. What they did not find was detectable employment or wage effects at the occupation or industry level. Hampole et al. reached a similar conclusion in a 2025 NBER paper, finding that tasks with higher AI exposure saw reduced labor demand, while AI exposure still showed no detectable relationship to overall employment or wages at the occupation or industry level. A Federal Reserve note using Lightcast postings and Census BTOS data likewise found no evidence through late 2025 that industries or firms with higher AI adoption were posting fewer jobs in total, though… it cautioned that occupation-specific displacement may be hiding beneath the aggregate calm.

The central analytical point is that reorganization is not the same thing as aggregate destruction. The labor market can change in meaningful ways long before the topline data fully registers the shift.

There is another wrinkle, and it complicates the popular story that women are automatically the first casualties of AI. In an IMF working paper, Huang found that places with higher AI adoption experienced larger declines in employment-to-population ratios. But the negative effect was concentrated in manufacturing, low-skill services, middle-skill workers, non-STEM occupations, and workers at the ends of the age distribution. Crucially, the adverse effect was more pronounced for men than for women. So the first realized employment effects that show up in the U.S. data are not uniformly anti-female.

While exposure tells us where risk could emerge, actual outcomes depend on sectoral adoption, local demand, complementarity, and how firms choose to adjust.

Still, it would be a mistake to take today’s aggregate wage null results as reassurance, since wage effects often lag task restructuring. Evidence from Denmark by Humlum and Vestergaard found precise null effects on earnings and hours two years after chatbot diffusion even as work was clearly being reorganized. Because the evidence is not U.S.-based, it cannot settle the U.S. question. But it does offer a useful methodological warning that work can change faster than pay.

This Becomes a Management Problem

Employer policy is where this becomes a management problem. The New York Fed’s 2026 Survey of Consumer Expectations found that 39% of employed respondents had used AI tools at work in the previous year. About 38% of employed respondents said AI training was important. Only 15.9% said their employer offered it. 37% said their workplace did not offer AI tools at all, and another 11% said the employer prohibited them…

Those numbers should seriously embarrass some executives! Some crazy macro-mismatches…

Taken together with the earlier sections, the real risk is a widening split that just does not get enough national discussion, rather than a single, clean “AI hurts women” outcome.

Women in AI-complementary professional roles may do well. But women in clerical and administrative roles may face restructuring pressure with weak adaptation pathways. Men will not all win, especially in exposed non-STEM and cyclical sectors. But men remain disproportionately positioned to capture the technical upside, where firms are already paying up for the capabilities closest to AI deployment and control.

This is why the current moment deserves more discipline than either the cheerleaders or the doomsayers are offering. The best evidence through early 2026 supports a measured but urgent conclusion… In the United States, AI investment is likely already altering gender inequality at work by redistributing exposure, adoption, and the skills employers reward, even if it has not yet clearly emerged as a driver of the overall gender pay gap.

That is the architecture of tomorrow’s labor market, being built in real time.

However, business leaders still have room to alter the outcome!

They can widen access to AI tools instead of hoarding them in technical enclaves;

They can offer training before workers fall behind instead of after; and,

They can build career ladders that move women into AI-complementary roles rather than waiting to discover, a few years from now, that the office was automated and the upside went elsewhere.

And guess what? Companies that tend to behave in such ways, are those most likely to see improved retention and productivity! (Here, here, here, and here, have at it)

So, no… the pay gap data has not delivered a final verdict. But the labor market has definitely begun writing one.

Endnote re how firms are already shifting the skill mix they reward: Babina et al. show that U.S. firms investing in AI move toward more educated workforces, more undergraduate and graduate degree holders, more STEM specialization, and more IT skills. They also find flatter hierarchies, with relatively more junior workers and fewer middle-management and senior roles. Demand rises for highly educated workers and those with STEM or IT backgrounds while some finance and maintenance skills lose ground. While this is not itself a gender estimate, when men remain overrepresented in many of the AI-complementary technical pathways, the composition effect is hard to ignore.

Sources:

Acemoglu, Daron, David Autor, Jonathon Hazell, and Pascual Restrepo. “Artificial Intelligence and Jobs: Evidence from Online Vacancies.” Journal of Labor Economics 40, no. S1 (April 2022). https://economics.mit.edu/sites/default/files/publications/AI%20and%20Jobs%20-%20Evidence%20from%20Online%20Vacancies.pdf.

Aldasoro, Iñaki, Olivier Armantier, Sebastian Doerr, Leonardo Gambacorta, and Tommaso Oliviero. “The Gen AI Gender Gap.” BIS Working Papers No. 1197, Monetary and Economic Department, Bank for International Settlements, July 2024. https://www.bis.org/publ/work1197.pdf.

Babina, Tania, Anastassia Fedyk, Alex X. He, and James Hodson. “Firm Investments in Artificial Intelligence Technologies and Changes in Workforce Composition.” NBER Working Paper No. 31325, June 2023. https://www.nber.org/papers/w31325.

Bick, Alexander, Adam Blandin, and David J. Deming. “The Rapid Adoption of Generative AI.” NBER Working Paper No. 32966, September 2024, revised February 2025. https://www.nber.org/system/files/working_papers/w32966/w32966.pdf.

Brynjolfsson, Erik, Danielle Li, and Lindsey Raymond. “Generative AI at Work.” The Quarterly Journal of Economics 140, no. 2 (May 2025): 889–942. Published February 4, 2025. https://academic.oup.com/qje/article/140/2/889/7990658.

Hampole, Menaka, Dimitris Papanikolaou, Lawrence D. W. Schmidt, and Bryan Seegmiller. “Artificial Intelligence and the Labor Market.” NBER Working Paper No. 33509, February 2025, revised September 2025. https://www.nber.org/papers/w33509.

Hashim, Ali, Gizem Kosar, and Wilbert van der Klaauw. “Use of Gen AI in the Workplace and the Value of Access to Training.” Liberty Street Economics, April 14, 2026. https://libertystreeteconomics.newyorkfed.org/2026/04/use-of-gen-ai-in-the-workplace-and-the-value-of-access-to-training/.

Huang, Yueling. “The Labor Market Impact of Artificial Intelligence: Evidence from US Regions.” IMF Working Paper No. 2024/199, September 2024. https://www.imf.org/-/media/files/publications/wp/2024/english/wpiea2024199-print-pdf.pdf.

Humlum, Anders, and Emilie Vestergaard. “Still Waters, Rapid Currents: Early Labor Market Transformation under Generative AI.” NBER Working Paper No. 33777, May 2025, revised March 2026. https://www.nber.org/papers/w33777.

Kochhar, Rakesh. “Which U.S. Workers Are More Exposed to AI on Their Jobs?” Pew Research Center, July 26, 2023. https://www.pewresearch.org/social-trends/2023/07/26/which-u-s-workers-are-more-exposed-to-ai-on-their-jobs/.

Kinder, Molly, Xavier de Souza Briggs, Mark Muro, and Sifan Liu. “Generative AI, the American Worker, and the Future of Work.” Brookings Institution, October 10, 2024. https://www.brookings.edu/articles/generative-ai-the-american-worker-and-the-future-of-work/.

Otis, Nicholas G., Solène Delecourt, Katelyn Cranney, and Rembrand Koning. “Global Evidence on Gender Gaps and Generative AI.” Harvard Business School Working Paper No. 25-023, 2025. https://www.hbs.edu/ris/Publication%2520Files/25023_52957d6c-0378-4796-99fa-aab684b3b2f8.pdf.

Schendstok, Matt, and Sydney Schreiner Wertz. “Occupational Exposure to Artificial Intelligence by Geography and Education.” Office of Economic Policy Working Paper 2024-02, April 2024. https://home.treasury.gov/system/files/136/AI-Combined-PDF.pdf.