Who's Really Deciding Whether You Buy a House?

by Mardoqueo Arteaga

AI;DR: Consumer sentiment just hit a record low and the Fed is expected to hold rates steady this week. For prospective homebuyers, the uncertainty isn't going away anytime soon. In environments like this, the voices around you get louder—partners, parents, friends, cultural scripts. Understanding who's actually shaping your decision is the first step to making one you won't regret.

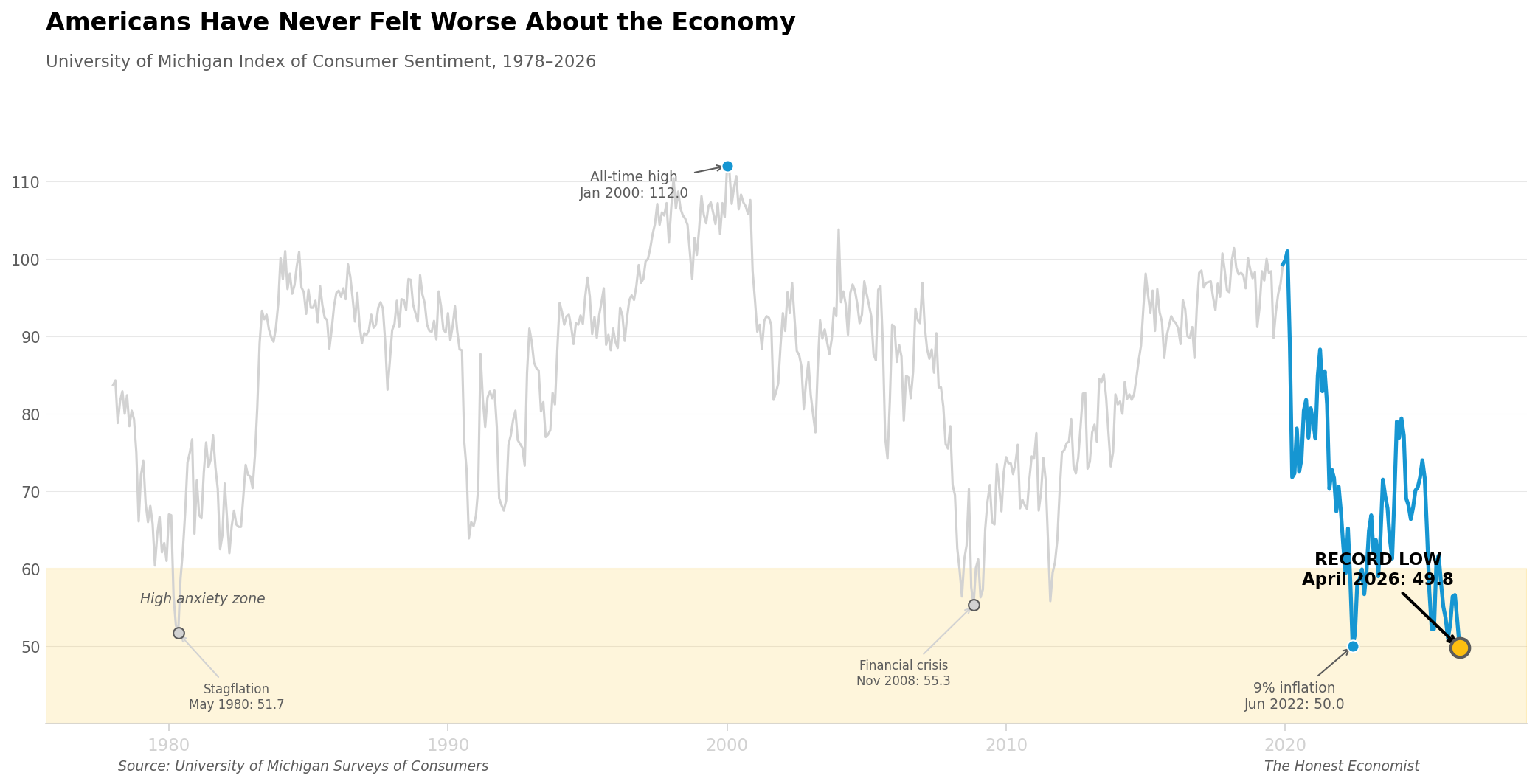

Consumer sentiment fell to 49.8 in April. That is the lowest reading since the University of Michigan began tracking it in 1978! It’s lower than June 2022, when inflation peaked at 9%, and lower than the early months of the pandemic. The Iran conflict, rising gas prices, and a sharp increase in inflation expectations have combined to produce a level of economic anxiety that the survey is now calling historic.

This week, the Federal Reserve meets to decide on interest rates. Markets expect the FOMC to hold steady. Before the war, traders anticipated a cut in June; now that timeline is uncertain. Year-ahead inflation expectations jumped from 3.8% to 4.7% in a single month, the largest increase since April 2025. The Fed is watching, and so is everyone trying to make a major financial decision.

For prospective homebuyers, this means the noise isn't going away. Mortgage rates remain elevated. The macro environment offers no clear signal. And yet decisions still have to be made. The question is how to make them well when everything feels uncertain.

I've been thinking about this problem from an unusual angle. I spent the past week in London for work, and part of my time was spent in sessions on something called buying groups—a concept from B2B marketing that, I've come to believe, applies directly to how people decide whether to buy a home.

The Buying Group Framework

In B2B marketing, we know that purchase decisions are rarely made by a single individual. They are shaped by networks of influencers: colleagues who will use the product, managers who control budgets, executives who sign contracts, and advisors who shape opinion before the formal decision is ever made. The person who ultimately signs is often just the final node in a network that has already done most of the deciding.

Effective marketers understand this. They don't target only the decision-maker. They map the entire buying group and address each participant's concerns, because the decision is made collectively even when it appears individual.

Homeownership works the same way.

When someone is weighing whether to buy, they are not deciding in isolation. They are absorbing input from a network of influences: a partner who speaks about wanting "a place of our own," parents who transmit expectations about stability and adulthood, friends who recently purchased and narrate their experience, friends who have not and offer a different kind of validation, and a broader cultural script that equates ownership with maturity and renting with impermanence.

By the time a person sits down to "decide," the decision has already been shaped by voices that may never enter the formal calculus. The question, then, is not whether these influences exist. The question is whether they can be seen clearly.

The University of Michigan's Index of Consumer Sentiment fell to 49.8 in April 2026, lower than the 2008 financial crisis, lower than the stagflation of 1980, lower than the peak inflation of June 2022. This is the worst Americans have felt about the economy since the survey began. Source: University of Michigan Surveys of Consumers. Tune in soon for a conversation about polls vs markets, which have grown in popularity.

Why This Matters Now

When consumer sentiment is high and the economic outlook is stable, the buying group's influence is less consequential. Most of the voices are saying similar things, and the macro environment provides a clear backdrop against which to evaluate personal circumstances.

When sentiment craters and uncertainty spikes, the dynamics change. The voices get louder. They also get more divergent. Some urge caution; others urge action before conditions worsen. The cultural script about ownership (which, mind you, has been internalized over decades) continues to exert pressure even when the current environment looks nothing like the one in which that script was written.

The Fed's expected decision this week illustrates the challenge. If rates hold steady, mortgage rates stay elevated. The environment that has made housing decisions difficult for the past two years continues, and I wrote about in the prior installment about why 50 million Americans are currently staying put. In other words, there is no external signal that resolves the uncertainty. The decision remains with the individual and with the buying group surrounding them.

In this context, clarity about who is shaping the decision becomes unusually valuable.

Evaluating the Voices

Not all influences are equally well-calibrated to current conditions.

Parents often have strong views about homeownership. Those views were frequently formed in an economy where the median home cost three times the median income. Today that ratio is closer to seven nationally, and significantly higher in major metropolitan areas. The advice may still be sound, but it requires contextualizing for a different structure.

Friends who recently purchased are valuable sources of information about the process. They are also, by necessity, invested in believing their decision was correct. Their enthusiasm is data, but it is data about their situation and their psychology, not a recommendation for someone else's circumstances.

The cultural script of ownership as milestone, renting as transience is powerful precisely because it operates below conscious awareness. It was encoded in an era of stable rates, predictable appreciation, and long tenure in single locations. For many people, it remains correct. For others, particularly those in high-cost markets or volatile career paths, it may not apply as directly.

I notice these dynamics in my own thinking. Parents of friends and colleagues of mine have clear expectations about ownership, expectations shaped by an economy I did not experience. My graduate training was in household expectations and belief formation (aka the study of how people absorb and transmit economic signals) and yet I find myself subject to the same pressures I analyze. The transmission mechanism operates on the researcher as much as the researched.

Making a Decision That Sticks

The goal here is not to silence the buying group. The influences exist, and many of them contain genuine insight. The goal is to see them clearly enough to weigh them appropriately. A few questions that may help:

What is this person's actual knowledge of my financial situation? General advice about ownership may not account for specific debt loads, income variability, or timeline constraints.

Is this advice calibrated to my market? The calculus in a market where median homes cost $300,000 differs substantially from one where they cost $800,000.

Is this voice speaking from recent, relevant experience? Conditions in housing markets shift quickly. Advice from someone who purchased five years ago reflects a different rate environment.

Am I feeling pressure from a script, or from an analysis? The script says ownership is what adults do. The analysis asks whether ownership makes sense given specific circumstances.

Buyers who have examined their buying group and reached a clear conclusion, whatever that conclusion is, tend to make more confident decisions. They are less likely to experience doubt at inspection, less likely to second-guess offers, and more likely to close. Clarity about influences produces clarity about action.

Conclusion

The Fed will announce its decision on Wednesday. Markets expect rates to hold. For prospective homebuyers, this means the environment of uncertainty continues. There is no macro signal that will resolve the question of whether to buy.

What remains, however, is the work of understanding the decision itself: who is shaping it, what assumptions they carry, and whether those assumptions fit the current structure. In an economy where sentiment is at a historic low and the path forward is unclear, that understanding is the closest thing to solid ground.

The buying group will keep talking. Can you hear your own signal through the noise?

Sources:

University of Michigan. "Surveys of Consumers: April 2026 Final Results." April 25, 2026.

Board of Governors of the Federal Reserve System. "FOMC Statement." March 18, 2026.

CME Group. "FedWatch Tool." Accessed April 27, 2026.

Goodman, Laurie S. and Christopher Mayer. "Homeownership and the American Dream." Journal of Economic Perspectives, 2018.