The 114-Word Central Bank

by Mardoqueo Arteaga

AI;DR: Kevin Warsh closed his first FOMC meeting with the shortest post-meeting statement of the every-meeting era and a flat refusal to offer forward guidance. Christopher Sims, the 2011 Nobel laureate, formalized the framework that explains why this may be the right call for most of the population, and why it will not land the same way for everyone. Rational inattention starts from a physical fact: people process information at finite bits per second and allocate that capacity optimally across competing signals. Households, whose optimal signal from the Fed is approximately one bit, will not notice the missing words. Markets, which read every syllable, will find the remaining ones more consequential. The same framework explains why 42 percent of the world now actively avoids the news. The binding constraint is the channel, not the content.

Statements that Stop Explaining

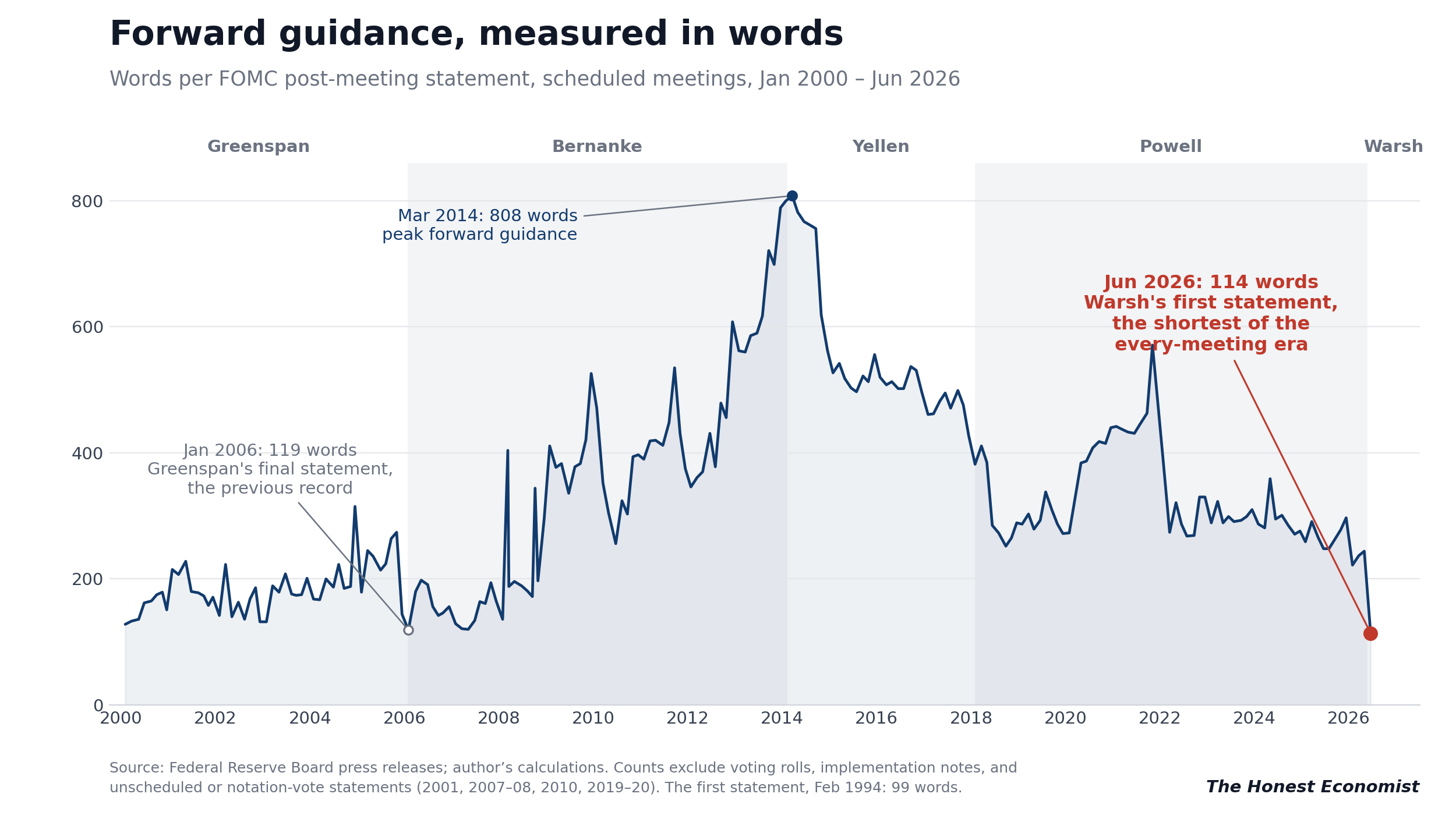

On June 17, Kevin Warsh closed his first meeting as Federal Reserve chairman with a statement of 114 words. By my count, it is the shortest statement to follow a scheduled FOMC meeting since the Committee began issuing one after every meeting in January 2000. The previous record belonged to Alan Greenspan's final statement, in January 2006, at 119 words. Five days after Warsh's release, Greenspan's death at 100 was announced.

The numbers trace a 26-year round trip. The first statement the Fed ever issued, in February 1994, ran 99 words, a figure the Board's own researchers report in a 2015 FEDS note on the semantics of the statement. Statements lengthened through the 2000s, then swelled after 2008 as the statement itself became the policy instrument, peaking at 808 words in March 2014, the meeting at which the Committee retired its unemployment threshold in favor of qualitative guidance. The Powell-era average settled near 330. Warsh cut that by more than half in a single meeting. He also declined to submit his own projection to the dot plot, announced five task forces to review the Fed's operations, and described the new statement at his press conference as shorter, simpler, and stripped of older language. The final substantive sentence is six words: "The Committee will deliver price stability."

A methodology note, because the press counted differently: CNBC put the June statement at 130 words against 341 in April. Those counts include the vote-tally preamble. The series above excludes voting rolls and implementation notes, consistent with the Board's 2015 FEDS note, which my counts reconcile to within two words. On the same texts, the June statement reads at roughly a twelfth-grade level on the Flesch-Kincaid index, the first post-meeting statement near a high-school reading level in about two decades. The 2013 vintage required roughly three years of study beyond a bachelor's degree, a complexity pattern Hernández-Murillo and Shell documented at the St. Louis Fed in 2014.

Two weeks after the meeting, at the ECB's annual forum in Sintra, a moderator tried to extract a rate path. Warsh refused twice in one sentence: "No forward guidance, no forward guidance." Christine Lagarde volunteered that her one regret as ECB president was to have felt bound and compelled by forward guidance, and the governors of the Bank of England and the Bank of Canada said they oppose the practice as well. Jeffrey Roach at LPL Financial read the June statement as a return to the deliberately minimalist Greenspan style once called constructive ambiguity.

Christopher Sims would recognize the moment. He shared the 2011 Nobel Prize with Thomas Sargent for empirical work on cause and effect in the macroeconomy, but his 2003 paper on rational inattention, a smaller and stranger contribution, may prove the more durable one (and one that inspired my own dissertation research). It explains why most of the country never read the 808-word statements. It also predicts, less comfortably for the new chairman, that the audience that did read them will not simply shrug at their disappearance.

The Channel Capacity Constraint

I argued in an earlier post that the transmission mechanism from FOMC statements to household behavior resembles a lossy functor, structure-preserving in theory but structure-destroying in practice. Sims gives that intuition a formal foundation.

The setup: a person must choose an action that depends on a state variable X, such as the real interest rate or the inflation rate. The person cannot observe X directly. Instead, they choose a signal Y, a noisy function of X, subject to an information-processing constraint:

I(X; Y) ≤ κ

where I(X; Y) is the mutual information between the state and the signal, measured in bits, and κ is the agent's channel capacity. Mutual information, from Shannon's 1948 theory, quantifies the reduction in uncertainty about X achieved by observing Y. One bit corresponds to one yes-or-no distinction per period.

The key insight, and the reason Sims's framework is more powerful than generic bounded rationality, is that the person chooses the signal optimally. Given finite capacity, attention flows to whichever dimensions of the state matter most for the loss function. In the linear-quadratic-Gaussian case that Sims solves, the optimal signal makes the conditional distribution of X given Y Gaussian, with variance independent of the realization of Y. The result looks like a signal extraction problem with endogenous noise: the variance of the error is set by the agent's capacity and the statistical properties of X, not by an exogenous physical noise process.

The Attention Allocation Problem

Sims observed, with characteristic dryness, that he pages through the business section of the New York Times most mornings, sees the charts and tables of financial data, and most days takes no action on any of it. I mean, I do the same. Do you?

Consider the typical household's information environment: the federal funds rate, CPI inflation, the local labor market, grocery prices, mortgage rates, equity returns, tariff announcements, immigration policy, AI disruption. Each is a state variable with some bearing on household decisions, and each competes for a share of a fixed κ.

The comparative statics deliver a clean prediction in that agents allocate more attention to state variables that are more volatile, more consequential for their loss function, and more persistent. A one-time tariff announcement is volatile and consequential but not persistent, since the policy may reverse. For example, CPI inflation is persistent but was, until 2021, low-volatility. The federal funds rate is consequential for mortgage holders and nearly irrelevant for renters (not to disregard the enthusiasts in my audience, of course!). The framework predicts heterogeneous attention allocation across the population, which is what the data show.

Maćkowiak, Matějka, and Wiederholt's 2023 review in the Journal of Economic Literature confirms the pattern at the firm level: firms devote disproportionate attention to idiosyncratic shocks relative to aggregate shocks, because idiosyncratic variation is larger and more directly actionable. Firms respond quickly to their own demand shifts and sluggishly to monetary policy because the aggregate signal is small relative to the noise, so the optimal channel allocates it little capacity.

Implications for Central Bank Communication

The monetary policy implication follows directly, and Sims drew it himself. Financial market participants attend to every nuance of Fed communication; their loss functions are steep in the state variable, so their κ for this signal is high. Ordinary people react sluggishly, in effect compressing the policy statement through their own information-processing filters, whether the input is dense or simple.

That is a hard constraint on forward guidance as a tool for shaping household expectations. Forward guidance works only if agents process and act on it, and the typical household's optimal signal from the Fed is approximately one bit: rates going up, or rates going down. The dot plot, the Summary of Economic Projections, the calibrated language about substantial further progress, all of it passed through a one-bit channel and emerged as a binary that may or may not have matched what the Committee intended to communicate.

The experimental evidence is consistent. Maćkowiak and Wiederholt's 2025 work brings information provision experiments, randomized surveys that hand subjects information about inflation and measure belief updates, into the rational inattention framework. Two effects counteract: the experiment supplies a signal the subject would not otherwise have, raising the measured treatment effect, while the subject rationally reduces day-to-day attention to the variable, lowering the effect outside the survey. Weber and coauthors, surveying inflation expectations across multiple countries in 2025, find that information telling respondents something they do not already know moves beliefs far more than information confirming priors, exactly what the rational inattention model predicts.

Warsh's Natural Experiment

The new chairman is now testing the proposition in production, and the framework says the results will be asymmetric. The asymmetry is the testable content.

For households, the prediction is that nothing happens. The marginal 200 words of a Powell-era statement never cleared the one-bit channel, so their removal is unobservable from inside the constraint. The dispersion of household inflation expectations in the University of Michigan Surveys of Consumers and the New York Fed's Survey of Consumer Expectations should show no break at the June meeting.

Markets are the opposite case. Fed-watchers are the high-capacity agents in Sims's model, the ones whose loss functions justify professional bandwidth on every syllable. Withdrawing guidance from them does not reduce their attention. It raises the information value per remaining word and shifts the inference burden from the statement to the press conference, the speeches, and the minutes. Conditional uncertainty rises exactly where processing capacity is most concentrated. The prediction is higher implied rate volatility around FOMC dates, visible in instruments like the ICE BofA MOVE index, wider dispersion in professional forecasts, and a revival of the Greenspan-era cottage industry of exegesis. I suppose my point is that constructive ambiguity did not shrink Fed-watching in the 1990s.

The Feed Is Running the Same Experiment

A news feed is a signal: a curated stream the platform selects from the state space of everything happening in the world. The user processes it subject to κ. The platform's algorithm optimizes the signal for engagement. The user optimizes something else entirely, staying informed enough to make good decisions without exhausting the processing budget. The two objective functions are not aligned, and the gap widens as the environment gets noisier.

When the informational environment deteriorates, more tariff announcements, more policy reversals, more contradictory guidance, the rational response is not to process more information. It is to raise the threshold for acting on any signal. The agent coarsens the channel, collapsing fine-grained tracking into binary categories: things are basically fine, or things are basically not. This is the sluggish, lumpy pattern Sims predicted, and it is the same lumpiness Klenow and Kryvtsov documented in consumer price adjustment in 2008, long stretches of inaction punctuated by discrete jumps.

The aggregate evidence now has a number attached. The Reuters Institute's 2026 Digital News Report, fielded in January and February across 48 markets and roughly 100,000 respondents, puts global news avoidance at 42 percent, up from 29 percent when the series began in 2017. The United States sits at 45 percent. Trust in news stands at 37 percent, the lowest reading since the Institute began measuring it in 2015. In the rational inattention framework, this is not a vague malaise called information overload. Overload is precisely characterized: the mutual information required to track all relevant state variables exceeds κ, forcing a reallocation that drops some variables entirely. Tariff coverage gets dropped in favor of grocery prices. Forward guidance gets dropped in favor of the mortgage rate on a Zillow listing.

I see the same mechanism in the LinkedIn engagement data I work with (occupational hazard). Users engage less with economy-news content during periods of maximum policy volatility, the opposite of what a naive engagement model predicts. The rational inattention account is straightforward: when a state variable becomes more volatile and more transient at the same time, today's announcement reversed tomorrow, the present value of processing it falls, and the optimal bandwidth allocation moves elsewhere. The gap between smooth behavior and a volatile information environment is an attention tax on the economy, a real resource cost that appears nowhere in the national accounts.

The Takeaway

For the Fed: shorter is not dumber. A 114-word statement respects a constraint that 808 words could never buy through. But the framework licenses simplicity, not silence, and the two are worth keeping separate. For households, the withdrawn words were never arriving. For the high-capacity audience, the withdrawal is real, and its cost will show up as volatility priced around meetings rather than as confusion in survey expectations. The task forces should measure both.

For platforms: declining news engagement is not a content quality problem or an algorithm problem. It is a rational response to a deteriorating signal-to-noise ratio in the policy environment. Users are optimizing. The algorithm's objective function is not theirs.

The optimal response to a noisy, transient, rapidly reversing signal is to reduce the bandwidth allocated to it and wait for the persistent component to reveal itself. That was always the theory. As of June 17, it seems to be the official policy at the Fed. The rest of the feed is still fighting it.

Sources:

Academic literature

Sims, Christopher A. (2003), "Implications of Rational Inattention," Journal of Monetary Economics 50(3): 665-690. https://doi.org/10.1016/S0304-3932(03)00029-1

Shannon, Claude E. (1948), "A Mathematical Theory of Communication," Bell System Technical Journal 27(3): 379-423 and 27(4): 623-656. https://onlinelibrary.wiley.com/doi/10.1002/j.1538-7305.1948.tb01338.x

Maćkowiak, Bartosz, Filip Matějka, and Mirko Wiederholt (2023), "Rational Inattention: A Review," Journal of Economic Literature 61(1): 226-273. https://www.aeaweb.org/articles?id=10.1257/jel.20211524

Maćkowiak, Bartosz, and Mirko Wiederholt (2026), "Rational Inattention during a Randomized Controlled Trial," American Economic Review: Insights 8(1): 19-35. https://www.aeaweb.org/articles?id=10.1257/aeri.20240509. Earlier version: ECB Working Paper No. 3054 (2025), https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5252109

Weber, Michael, Bernardo Candia, Hassan Afrouzi, Tiziano Ropele, Rodrigo Lluberas, Serafin Frache, Brent Meyer, Saten Kumar, Yuriy Gorodnichenko, Dimitris Georgarakos, Olivier Coibion, Geoff Kenny, and Jorge Ponce (2025), "Tell Me Something I Don't Already Know: Learning in Low- and High-Inflation Settings," Econometrica 93(1): 229-264. https://onlinelibrary.wiley.com/doi/full/10.3982/ECTA22764

Klenow, Peter J., and Oleksiy Kryvtsov (2008), "State-Dependent or Time-Dependent Pricing: Does It Matter for Recent U.S. Inflation?" Quarterly Journal of Economics 123(3): 863-904. https://doi.org/10.1162/qjec.2008.123.3.863

Hernández-Murillo, Rubén, and Hannah G. Shell (2014), "The Rising Complexity of the FOMC Statement," Federal Reserve Bank of St. Louis Economic Synopses, No. 23. https://research.stlouisfed.org/publications/economic-synopses/2014/11/05/the-rising-complexity-of-the-fomc-statement/

Acosta, Miguel, and Ellen E. Meade (2015), "Hanging On Every Word: Semantic Analysis of the FOMC's Postmeeting Statement," FEDS Notes, Board of Governors of the Federal Reserve System, September 30. https://www.federalreserve.gov/econresdata/notes/feds-notes/2015/semantic-analysis-of-the-FOMCs-postmeeting-statement-20150930.html

Federal Reserve and Official Sources

Federal Open Market Committee (2026), "Federal Reserve Issues FOMC Statement," June 17. https://www.federalreserve.gov/newsevents/pressreleases/monetary20260617a.htm

Board of Governors of the Federal Reserve System (2026), "Kevin Warsh Takes Oath of Office as Chairman," May 22. https://www.federalreserve.gov/newsevents/pressreleases/other20260522a.htm

Federal Reserve Board, FOMC historical materials by year (statement archive used for word counts). https://www.federalreserve.gov/monetarypolicy/fomc_historical_year.htm

Press Coverage of the Warsh Transition

CNBC (June 17, 2026), "Fed Holds Rates Steady in Kevin Warsh's First Meeting as Chairman." https://www.cnbc.com/2026/06/17/fed-interest-rate-decision-june-2026.html

CNBC (June 17, 2026), "June Fed Meeting: Here's What Changed in the New Statement." https://www.cnbc.com/2026/06/17/june-fed-meeting-redline.html

CNN Business (July 1, 2026), "Kevin Warsh's Reform-Focused Approach Is Already Winning Support on the Global Stage." https://www.cnn.com/2026/07/01/economy/fed-chairman-warsh-first-global-speech

U.S. News & World Report (June 22, 2026), "Warsh Begins a New Era at the Federal Reserve." https://www.usnews.com/news/national-news/articles/2026-06-22/warsh-begins-a-new-era-at-the-federal-reserve

Media Environment Data

Reuters Institute for the Study of Journalism, University of Oxford (2026), Digital News Report 2026. https://reutersinstitute.politics.ox.ac.uk/digital-news-report/2026. Executive summary: https://reutersinstitute.politics.ox.ac.uk/digital-news-report/2026/dnr-executive-summary

Data and Replication

FOMC statement word counts and Flesch-Kincaid grade levels: author's calculations on Federal Reserve statement texts, January 2000 through June 2026. Counts exclude voting rolls, implementation notes, and unscheduled or notation-vote statements; the methodology reconciles with Acosta and Meade (2015) to within two words on overlapping observations. Statement corpus assembled from the Federal Reserve's website; an automatically updated public archive is maintained at https://github.com/vtasca/fed-statement-scraping.