The Fed’s Balance-Sheet Fight Is Bigger Than One Rate Decision

by Kent O. Bhupathi

AI;DR: The article argues that Kevin Warsh’s early Fed leadership should be judged less by his June 2026 decision to hold rates steady and more by his decision to launch a review of the Fed’s balance-sheet framework. The balance sheet is presented as a core operating system of modern monetary policy, affecting duration risk, bank reserves, repo markets, Treasury financing, mortgage credit, and the Fed’s control over short-term rates. While a smaller portfolio could reduce market distortions, clarify fiscal-monetary boundaries, lower political pressure, and preserve room for future crisis action, the article stresses that further shrinkage carries real financial-plumbing risks, especially around reserve scarcity, payment-system needs, and repo-market capacity. The central claim is that the post-QE (quantitative easing) Fed now faces a structural design problem: determining how small the balance sheet can safely become, what reserve regime it should operate, and how to recalibrate the machinery of monetary policy without triggering market dysfunction.

Federal Reserve meetings have a ritual quality. Traders stare at screens. Reporters reach for the same three verbs: held, cut, raised. Business leaders pretend they are not refreshing their feeds while doing exactly that. In Kevin Warsh’s first stretch as Fed chair, the question hanging over the room was simple enough for a headline. Would he move rates?

He did not. In June 2026, Warsh held the federal funds target range at 3.5 to 3.75%, calming immediate anxiety around his early leadership. The policy rate still matters. It shapes borrowing costs, asset prices, mortgage math, investment decisions, and the daily emotional weather of anyone financing anything larger than lunch.

But Warsh then sent the more consequential signal through a less dramatic move. He created a task force to review the Federal Reserve’s balance-sheet framework. This can carry real force.

The Fed’s balance sheet holds the securities portfolio the central bank accumulated through years of quantitative easing and then tried to shrink through quantitative tightening. The portfolio shapes how much duration risk private investors absorb, how much liquidity banks hold, how repo markets function, and how reliably the Fed can keep short-term rates within its target range.

And we best be paying attention to the timeline…

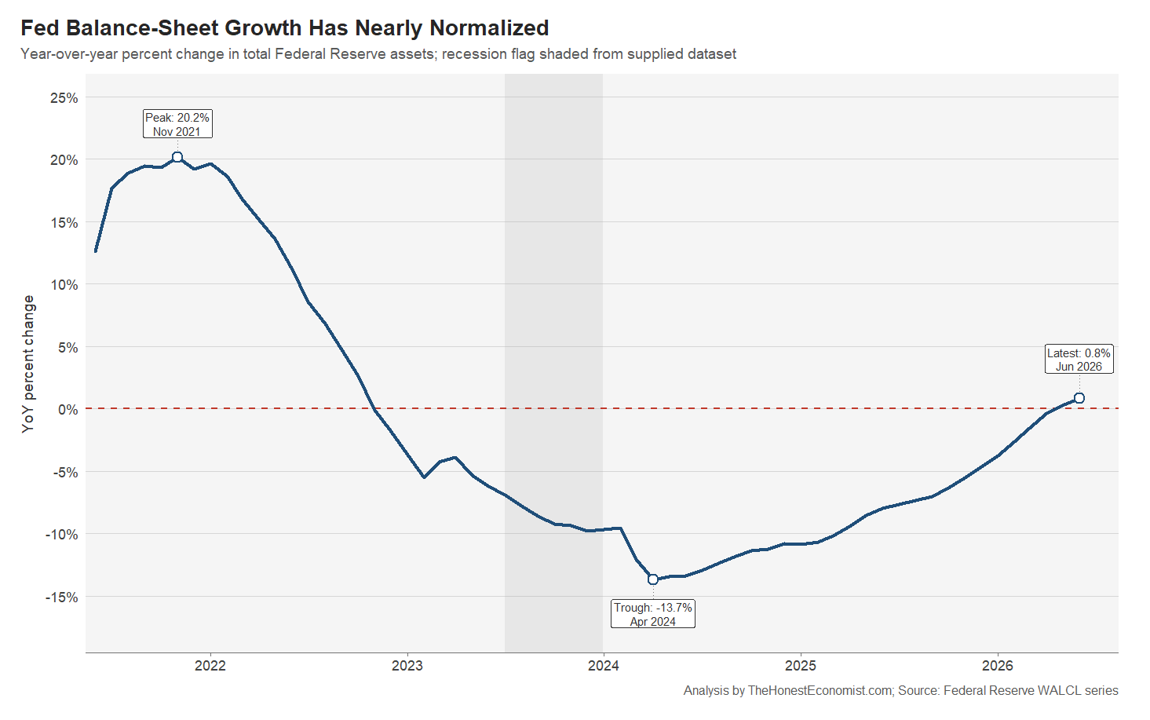

The Fed ended quantitative tightening on December 1, 2025. Ten days later, after officials judged reserves ample, the Fed began buying shorter-term Treasury securities to manage reserve levels. By March 25, 2026, total assets had increased by $49 billion from September 2025 to about $6.7 trillion. The weekly WALCL series reached roughly $6.725 trillion on July 1, 2026.

The Fed’s own reserve-management policy drove that increase after QT reached the ample-reserves floor. Warsh kept runoff paused in June, reaffirmed the ample-reserves approach, and ordered a review.

The rate decision may have eased the immediate anxiety, but the balance-sheet task force exposed the deeper fight.

The Balance Sheet Is the Operating System

The easy mistake is to treat the balance-sheet debate as Plan B. Warsh held rates steady, the thinking goes, so he turned to the bond portfolio instead. That reading has surface appeal, but it gets the decision wrong if done hastily.

Rates and the balance sheet interact, but they are not interchangeable buttons. The policy rate works through the short end of the curve and expectations about future monetary policy. Balance-sheet policy works through securities supply, term premia, market liquidity, reserve balances, repo financing, and the institutional machinery that lets the Fed implement policy. It is less like turning a dial than changing pressure in a financial water system. The pipes have opinions.

Governor Stephen Miran made the clearest official 2026 case for shrinking the balance sheet in March, before Warsh’s June press conference. Miran argued that a smaller portfolio could reduce market distortions, lower remittance volatility, protect the boundary between fiscal and monetary policy, and rebuild “dry powder” for the next crisis. He also stressed that any renewed shrinkage should move slowly, rely mainly on maturities rather than outright sales, and likely take years once the Fed prepared the implementation changes needed.

Warsh made a different move in June. He launched a review of the current ample-reserves regime and possible alternatives. He withheld any order to shrink the portfolio and directed the Fed to settle the operating framework it intends to use.

That distinction matters because the Fed has already passed the easy phase of balance-sheet reduction. The runoff that began in 2022 reached the ample-reserves floor by late 2025. After the Fed stopped QT and resumed modest Treasury purchases to maintain reserves, the debate shifted from runoff speed to steady-state design.

Fed staff have acknowledged that no consensus exists on the optimal steady-state size. Recent speeches and research show a real split. Some officials want a materially smaller footprint. Others think a fixation on shrinkage misunderstands the purpose of the ample-reserves system. The fight now concerns the operating system of post-2008 monetary policy.

Why a Smaller Portfolio Appeals

The strongest case for a smaller balance sheet is institutional. A smaller Fed portfolio could make monetary policy cleaner, reduce political friction, improve price discovery, and leave more room for future emergency action.

When the Fed holds a large stock of long-duration Treasuries and mortgage-backed securities, it removes duration risk from private markets. And that can compress long-term yields.

If the Fed holds fewer of those securities, private investors must absorb more duration risk, which should push term premia higher and make long rates reflect private risk-bearing constraints more fully. For borrowers, that can mean higher mortgage rates, higher corporate borrowing costs, and tighter financial conditions. For markets, it can mean prices driven less by central-bank absorption and more by actual private appetite.

The empirical literature supports that mechanism, though not as a crude “QE in reverse” story. Du, Forbes, and Luzzetti’s 2024 NBER cross-country study of seven advanced economies found that QT announcements raise government bond yields and steepen yield curves, with stronger effects when QT is active rather than passive. Smith and Valcarcel’s work on the 2017 to 2019 U.S. runoff found that QT tightened financial conditions mainly through implementation and liquidity effects. Lu and Valcarcel found that the 2022 episode looked different, with stronger announcement effects and a clearer signaling channel.

Newer high-frequency work by D’Amico and Seida sharpens the point. They find that Treasury-yield sensitivities to QT supply surprises can exceed sensitivities to QE surprises, even outside crisis conditions. Lloyd and Ostry similarly find that QT surprises since 2017 had larger and more persistent effects on Treasury yields than equal-sized QE surprises, partly through expectations for future short rates. Markets do not wait for runoff to finish before pricing what they think the Fed means.

And from a governance perspective A smaller portfolio could reduce the Fed’s role in mortgage-credit allocation through its MBS holdings. It could lower political heat around interest payments on large reserve balances, often perceived as subsidies to banks even when the mechanics are more complicated. It could also preserve more room for future QE if the economy again hits the effective lower bound.

Miran’s point about fiscal-monetary boundaries deserves attention. When the Fed owns a very large share of government securities, debt management and monetary policy can begin to look uncomfortably close. Treasury should make debt-management choices. The central bank should run monetary policy. Keeping those lanes distinct is part of institutional credibility.

So, shrinking the balance sheet has real appeal. And the Fed’s portfolio is not sacred. It grew through emergency choices, post-crisis operating changes, and pandemic-era interventions. A smaller footprint may be desirable. But a smaller house is easier to defend only if the load-bearing walls remain intact.

Fed balance-sheet growth peaked near +20% YoY in late 2021, marking the high point of the post-pandemic expansion cycle.

Quantitative tightening drove a sharp reversal, with YoY asset growth falling below zero in late 2022 and reaching roughly -14% by April 2024.

The balance sheet then moved from deep contraction toward stabilization, returning to roughly flat or slightly positive YoY growth by mid-2026.

The key policy question has shifted from whether the Fed can shrink its portfolio to what steady-state balance-sheet regime it should operate after QT.

The Plumbing Can Push Back

There are risks, of course. The Fed has already learned that reserves can look ample until they suddenly do not. The September 2019 repo-market disruption remains the central warning.

During the 2017 to 2019 normalization, reserves declined, repo-rate distortions increased, rate spikes became more likely, and payment-timing stress worsened. Copeland, Duffie, and Yang show how normalization strained the money-market machinery before the Fed was forced to intervene. Financial plumbing is boring only when it works.

Reserve demand is not a smooth line policymakers can estimate once and file away. Afonso, Giannone, La Spada, and Williams estimate that when reserves are above roughly 12 to 13% of bank assets, demand is satiated and reserves are abundant. Below that zone, the curve becomes increasingly sensitive as reserves move from ample toward scarce. The exact floor can shift with regulation, bank behavior, payment needs, Treasury issuance, and market stress.

QT can expose balance-sheet dependence that aggregate reserve measures miss. Acharya and coauthors argue that QE encouraged banks to expand deposit-like liquidity claims and credit commitments, while QT did not make those claims shrink in proportion. A system can look comfortable overall while specific institutions, funding channels, or markets become fragile.

Barr’s 2026 warning turns on payments. Banks with too few reserves may ration outgoing payments, creating bottlenecks, funding pressure, and financial-stability risks. Darrell Duffie makes the related point that the payment system itself puts a floor under the Fed’s balance sheet because banks need reserves to settle smoothly.

Anbil, Anderson, Cohen, and Ruprecht push the constraint beyond reserves. They argue that repo-market capacity, shaped by nonbank liquidity supply, may bind first. QT increases the Treasury financing burden on private markets while reducing system liquidity, so repo strain can appear before reserves look scarce. Their work also shows why rates and the balance sheet cannot be separated cleanly, since higher policy rates can expand repo capacity and support a smaller portfolio.

Runoff forces private investors to hold more Treasuries, raises repo financing demand, shifts flows between deposits and money funds, and changes reserve balances. Treasury issuance, the Treasury General Account, ON RRP balances, bank liquidity rules, and the policy-rate level all feed into the same machinery. The balance-sheet question stops looking like accounting once that machinery starts moving.

Nobody campaigns on repo-market capacity. Then one day, repo-market capacity campaigns on you.

Warsh’s Test Is Discipline Without Damage

Warsh’s early legacy will depend less on how quickly he cuts rates than on whether he can manage this redesign with discipline, transparency, and respect for complexity.

Powell’s pandemic-era QE began during an extraordinary emergency, alongside an unprecedented fiscal response. Those choices also helped create the monetary backdrop for one of the worst inflationary episodes in decades. The lesson is not paralysis in crisis. Emergency tools leave institutional residue. Balance sheets expand quickly and shrink slowly. Market structures adapt. Political narratives harden. Rescue can become architecture.

Warsh inherits the harder aftershock. He must decide how much of the crisis machine should remain. That decision will shape long-term yields, bank liquidity, mortgage markets, Treasury financing, money-market functioning, and the credibility of the Fed’s claim to serve the broad public interest.

Ultimately, the country does not need a Fed chair auditioning for ideological applause. It needs one who acts on data, market evidence, professional surveying work, and financial-stability analysis. Before the next round of shrinkage begins, the Fed needs answers to…

How much smaller can the balance sheet get while preserving ample reserves?

Does reserve demand set the floor, or does repo-market capacity bind first?

Should MBS runoff continue faster than Treasury runoff?

Should future QT remain passive, turn active, or include sales?

How can the Fed communicate balance-sheet changes without sending a false rate-path signal?

What changes to regulation, payment systems, dealer capacity, or standing liquidity facilities would make a materially smaller balance sheet safe?

Those questions are the substance of the review.

Further shrinkage may be feasible and desirable, true. A smaller portfolio could reduce distortions, clarify institutional boundaries, and leave the Fed less politically exposed. But balance-sheet reduction cannot be treated like decluttering. The Fed is recalibrating machinery that links the Treasury market, the banking system, money funds, repo dealers, mortgage finance, and the price of credit across the economy.

Warsh’s task force deserves your attention because the Fed’s next serious fight may concern the architecture of American central banking after the long age of QE, not one meeting’s rate decision. The bond portfolio now sits inside that architecture. Treating it as a side issue risks weakening the very framework the Fed relies on to control rates, stabilize markets, and preserve its credibility.

Sources:

Adam Copeland, Darrell Duffie, and Yilin Yang, Reserves Were Not So Ample After All, NBER Working Paper No. 29090 (Cambridge, MA: National Bureau of Economic Research, July 2021; revised August 2022), https://www.nber.org/papers/w29090.

Alyssa G. Anderson, Alessandro Barbarino, Anthony M. Diercks, and Stephen Miran, A User’s Guide to Reducing the Federal Reserve’s Balance Sheet, Finance and Economics Discussion Series (FEDS) 2026-019 (Washington, DC: Board of Governors of the Federal Reserve System, March 2026), https://www.federalreserve.gov/econres/feds/files/2026019pap.pdf.

Benjamin Eyal, Dave Na, and Arsenios Skaperdas, “A Decomposition of Balance Sheet Reduction,” FEDS Notes (Washington, DC: Board of Governors of the Federal Reserve System, February 2, 2026), https://www.federalreserve.gov/econres/notes/feds-notes/a-decomposition-of-balance-sheet-reduction-20260202.html.

Board of Governors of the Federal Reserve System, “Federal Reserve Issues FOMC Statement,” press release, May 1, 2024, https://www.federalreserve.gov/newsevents/pressreleases/monetary20240501a.htm.

Board of Governors of the Federal Reserve System, Monetary Policy Report – June 2025 (Washington, DC, June 20, 2025), https://www.federalreserve.gov/monetarypolicy/2025-06-mpr-part2.htm.

Board of Governors of the Federal Reserve System, “Federal Reserve Issues FOMC Statement,” press release, December 10, 2025, https://www.federalreserve.gov/newsevents/pressreleases/monetary20251210a.htm.

Burcu Duygan-Bump and R. Jay Kahn, “The Central Bank Balance-Sheet Trilemma,” FEDS Notes (Washington, DC: Board of Governors of the Federal Reserve System, January 14, 2026), https://www.federalreserve.gov/econres/notes/feds-notes/the-central-bank-balance-sheet-trilemma-20260114.html.

Chris Hughes and Joshua Younger, The Fed’s Ample Reserves Framework: A Report and a Response (Washington, DC: Brookings Institution, February 24, 2026), https://www.brookings.edu/articles/the-feds-ample-reserves-framework/.

Christopher J. Erceg, Marcin Kolasa, Jesper Lindé, Haroon Mumtaz, and Pawel Zabczyk, Central Bank Exit Strategies: Domestic Transmission and International Spillovers, IMF Working Paper No. 2024/073 (Washington, DC: International Monetary Fund, March 29, 2024), https://www.imf.org/en/Publications/WP/Issues/2024/03/29/Central-Bank-Exit-Strategies-Domestic-Transmission-and-International-Spillovers-546938.

Darrell Duffie, “The Payment System Puts a Floor on the Fed’s Balance Sheet,” Brookings, March 25, 2026, https://www.brookings.edu/articles/the-payment-system-puts-a-floor-on-the-feds-balance-sheet/.

Gara Afonso, Domenico Giannone, Gabriele La Spada, and John C. Williams, “Scarce, Abundant, or Ample? A Time-Varying Model of the Reserve Demand Curve,” Federal Reserve Bank of New York Staff Reports, no. 1019 (May 2022; revised November 2025), https://www.newyorkfed.org/research/staff_reports/sr1019.html.

Maxime Phillot, “US Treasury Auctions: A High-Frequency Identification of Supply Shocks,” American Economic Journal: Macroeconomics 17, no. 1 (January 2025): 245–73, https://doi.org/10.1257/mac.20210243.

Sriya Anbil, Alyssa Anderson, Ethan Cohen, and Romina Ruprecht, Beyond Reserves: The Federal Reserve’s Balance Sheet and the Repo Market, Finance and Economics Discussion Series (FEDS) 2026-041 (Washington, DC: Board of Governors of the Federal Reserve System, June 2026), https://www.federalreserve.gov/econres/feds/files/2026041pap.pdf.

Stefania D’Amico and Tim Seida, “Unexpected Supply Effects of Quantitative Easing and Tightening,” The Economic Journal 134, no. 658 (February 2024): 579–613, published September 12, 2023, https://doi.org/10.1093/ej/uead071.

Stephen I. Miran, “Prospects for Shrinking the Fed’s Balance Sheet,” speech at the Economic Club of Miami, Miami, FL, March 26, 2026, Board of Governors of the Federal Reserve System, https://www.federalreserve.gov/newsevents/speech/miran20260326a.htm.

Wenxin Du, Kristin Forbes, and Matthew N. Luzzetti, Quantitative Tightening Around the Globe: What Have We Learned?, NBER Working Paper no. 32321 (Cambridge, MA: National Bureau of Economic Research, April 2024), https://www.nber.org/papers/w32321.

Viral V. Acharya, Rahul S. Chauhan, Raghuram Rajan, and Sascha Steffen, Liquidity Dependence and the Waxing and Waning of Central Bank Balance Sheets, NBER Working Paper No. 31050 (Cambridge, MA: National Bureau of Economic Research, March 2023; revised December 2024), https://www.nber.org/papers/w31050.