The War Tax You're Already Paying

by Mardoqueo Arteaga

AI;DR: The Iran war has imposed an implicit tax on American households through higher gas prices. Unlike an actual tax, this one is regressive: the bottom 10% of earners spend nearly 4% of their income on gasoline, while the top 10% spend just 1.5%. The same price increase hits lower-income families three times harder. Oxford Economics estimates that if gas prices stay elevated, they will cost consumers $70 billion this year, more than offsetting the $60 billion boost from larger tax refunds. Consumer sentiment has already dropped to its lowest point of 2026, with the sharpest declines among households without stock portfolios. Compared to abstract macroeconomic shocks, this is a distributional one playing out at every gas station in America.

Three weeks ago, the average price of gasoline in the United States was $2.98 per gallon. Today it is $3.94. That is a 32% increase in 21 days.

The cause is straightforward. On February 28, the United States and Israel launched military operations against Iran. Iran responded by closing the Strait of Hormuz, a 21-mile channel through which roughly one-fifth of the world's oil supply flows. Global crude prices surged from $67 per barrel to over $100. American drivers absorbed the shock within days.

The policy debate will focus on strategy, on oil reserves, on whether the conflict was necessary. This post focuses on something simpler: who is paying for it right now, and how much.

The Math of a Regressive Shock

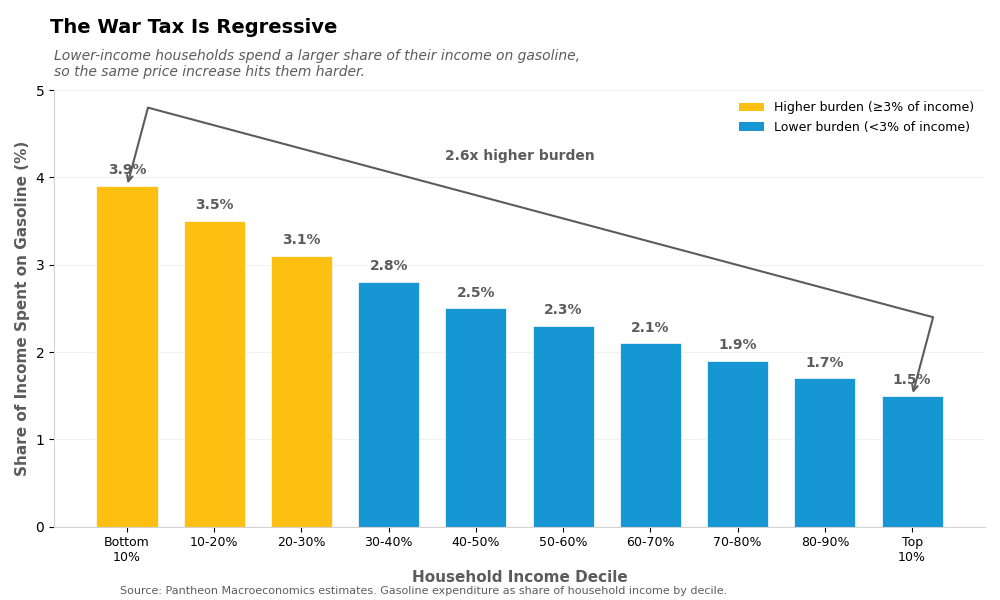

Not everyone experiences a gas price increase the same way. The reason is basic arithmetic. If you spend a larger share of your income on gasoline, a price increase takes a larger bite out of your budget.

Pantheon Macroeconomics estimates that the bottom 10% of American earners spend nearly 4% of their income on gasoline. The top 10% spend about 1.5%. This means the same $1 increase in gas prices hits a lower-income household roughly three times harder than a wealthy one, measured as a share of what they have to spend.

This pattern is what economists call regressive. A regressive tax takes a larger percentage from those who earn less. Sales taxes, for example, are regressive. Lottery tickets are regressive. And so is a global oil shock.

The same gas price shock hits lower-income households nearly three times harder than higher-income households, measured as a share of income.

The Aggregate Cost

Oxford Economics ran the numbers on what sustained high gas prices would mean for the American consumer. If gasoline averages $3.70 per gallon for the full year, American households will spend an additional $70 billion on fuel compared to pre-war projections.

For context, the Trump administration's tax cut legislation was expected to deliver roughly $60 billion in larger refunds this spring. The gas price shock has already eaten that and then some.

Bank of America's consumer spending data tells the same story from a different angle. In the week ending March 14, gasoline spending on the bank's credit and debit cards was up 14.4% year over year. Before the war, gas spending was running 5% below the prior year. That 20-percentage-point swing happened in two weeks.

The money going into gas tanks is money not going elsewhere. Gregory Daco, chief economist at EY-Parthenon, estimates that the gas price bump could push monthly inflation to 1% in March, the highest monthly increase in four years.

Who Feels It First

The University of Michigan's consumer sentiment survey offers a natural experiment. Interviews for the March release were conducted between February 17 and March 9. Roughly half were completed before the war began. Half were completed after.

The pre-war interviews showed improving sentiment. The post-war interviews erased those gains entirely. Consumer sentiment fell to 55.5, the lowest reading of 2026.

But the aggregate number hides the more telling pattern. Sentiment among households with significant stock holdings actually improved in recent months. Sentiment among households without equity exposure stagnated at depressed levels. Higher oil prices benefit shareholders in energy companies. They do not benefit families filling up a Honda Civic to get to work/school.

This is the K-shaped dynamic that analysts have described many times before, now playing out in real time. The same economy looks completely different depending on where you sit in the income distribution. The same war produces winners and losers, and the losers are disproportionately those who were already stretched thin.

Geography Compounds the Divide

The national average conceals enormous variation, so let me get more localized here. In California, drivers are paying $5.34 per gallon. In Louisiana, they are paying $3.20. Same war, same oil shock, same week. A 67% price difference.

California's higher prices reflect state taxes, environmental regulations, and refinery capacity constraints. Louisiana's lower prices reflect proximity to Gulf Coast production and refining infrastructure. Neither household chose these conditions. They inherited them.

For someone earning $40,000 a year and commuting 30 miles each way in a vehicle that gets 25 miles per gallon, the difference between California and Louisiana gas prices amounts to roughly $2,000 per year in additional fuel costs. That is real money, far too often the difference between making rent comfortably and not.

This geographic variation matters for anyone trying to understand consumer behavior at a local level. National inflation figures describe no one's actual experience. The household in Bakersfield and the household in Baton Rouge are living through different economic realities, even though the headline CPI is the same for both.

What Happens Next

The honest answer is that nobody knows. Federal Reserve Chair Jerome Powell said as much last week: "The economic effects could be bigger. They could be smaller. They could be much smaller or much bigger. We just don't know."

What we do know is that the current shock is already large enough to alter household behavior. Oxford Economics forecasts that 2026 will bring the slowest annual consumption growth since 2013, excluding the pandemic. Discretionary spending on travel, restaurants, and electronics is still growing, but it is not accelerating. Households are absorbing the gas shock by pulling back elsewhere.

The Century Foundation's Julie Margetta Morgan put it plainly: "You're seeing people who have maxed out their credit cards, are using 'buy now, pay later' to purchase their groceries. They're making it work for now, but that can fall apart quite quickly."

For policymakers, the implication is uncomfortable. Inflation had been declining for six consecutive months. Year-ahead inflation expectations had fallen to 3.4%, the lowest since early 2025. The war reversed that progress in a matter of days. The Fed now faces the familiar dilemma of supply shocks: raise rates to fight inflation and risk tipping a weakened consumer into recession, or hold steady and watch price expectations drift upward.

For households, the calculus is simpler. Every trip to the gas station is more expensive than it was a month ago. The war is far away. The bill is right here.

Sources:

American Automobile Association. "Gas Prices." AAA, 24 Mar. 2026.

Bank of America Institute. "Consumer Spending Data, Week Ending March 14, 2026." Bank of America, 21 Mar. 2026.

Hsu, Joanne. "Surveys of Consumers: Preliminary Results for March 2026." University of Michigan, 14 Mar. 2026.

Oxford Economics. "U.S. Consumer Outlook: Iran War Impact Assessment." Oxford Economics, 21 Mar. 2026.

Pantheon Macroeconomics. "Gasoline Expenditure by Income Decile." Pantheon Macroeconomics, Mar. 2026.

PBS NewsHour. "The Iran War and Surging Oil Prices Are Affecting Consumers." PBS, 10 Mar. 2026.

Yahoo Finance. "Gas Prices Are Just the Start: Consumers Will Feel More Pain from Iran War." Yahoo Finance, 21 Mar. 2026.